Seasonally adjusted general air cargo market performance data for July 2022 shows a continued slowing down of volume, load factor, capacity, and airfreight rates as the impact of economic and political uncertainties on world trade continues to hang over the industry.

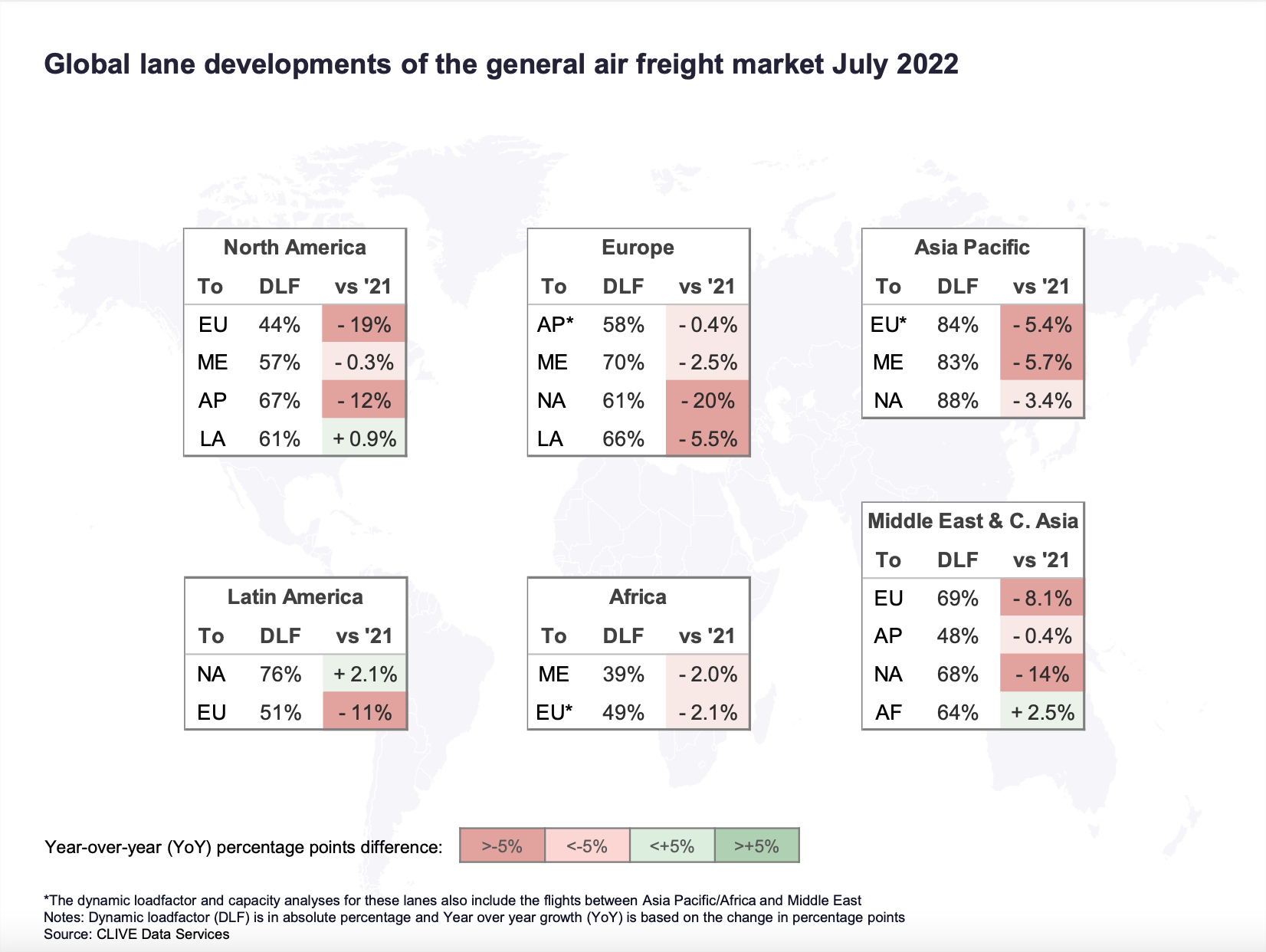

Weekly market intelligence from industry analysts, CLIVE Data Services, now part of Xeneta, shows volumes dropped 9% in the first month of the third quarter compared to July 2021. Demand was also down 9% versus the same month of 2019. Capacity growth slowed to just 4% over the July 2021 level and was 11% to July 2019. This caused CLIVE’S ‘dynamic load factor’ measure to drop 8% pts year-over-year to 58%.

Airfreight rates also continued to fall in July, relative to the June 2022 year-over-year analyses, CLIVE reports, although they remain at 121% versus July 2019 and 11% compared to the same month a year ago.

Read more: Air cargo tonnages and rates are both stabilising

The slowdown in the global air cargo market since March 2022 is ongoing, said Niall van de Wouw, founder of CLIVE and now Chief Airfreight Officer at Xeneta, with no let-up in the multitude of disruptions outside of the industry’s control. From uncertainties caused by the continuing war in Ukraine to the escalating ‘cost of living’ crisis and its impact on household budgets and business performance.

Latest reports in the Netherlands, for example, show supermarket rates for groceries 20% higher on average, compared to 11 months ago; further impacting the discretionary spending of consumers. Closer to home, airlines and airports continue to suffer severe operational challenges due to significant shortages of ground staff.

Read more: ‘Dark clouds’ hang over a slowing global air cargo market

“There are many dark clouds hanging over the air cargo industry given the state of the world right now. Volumes are subdued, and while air cargo rates are still elevated, they are slowly but surely easing back towards pre-Covid levels. From a rates point of view, indicators suggest the market has yet to bottom out. It’s clear that airlines are following the market very closely to ensure they are deploying their assets in the best possible way because the market is moving quickly. We have already seen freighters moving away from transatlantic routes.”

“The slow slides in rates, compared to 2019 and 2021, continues by a handful of percentages each month. In January, rates were 156% up compared to the same month in 2019. Now this figure is 121% or a reduction of 35% pts on a global scale. On the Atlantic, the decline in general airfreight rates we reported for the previous three months of 2022 continued in July. While this will be partly seasonal, the slight increase in load factor across the Atlantic relative to June – from 58% to 61% – might be a result of carriers and forwarders redirecting their freighter operations to other lanes, hence pushing up the load factor for the remaining flights on these routes,” he said.

{kind=link}